{kind=link}

{kind=link}

Don't have time to read it all right now?

Download your free PDF of "The Complete Guide to Credit Card Processing". Just give us your email and we'll send it to you right away!

Call us at 1(866) 607-4438

chapter

03

Being able to take mobile payments by accepting credit cards is great for small businesses, and there are a lot of payment processing options to choose from. As small business owners, finding a payment processing company who will work with you is challenging enough! But then how do you find a mobile payment processing company willing to work with you without crippling you with fees and eating into your bottom line? Let's look at our options together.

The mobile credit card reader itself is just one tiny piece of the puzzle. What's even more important is the mobile credit card processor you choose. Who you choose to use for your mobile credit card processing will depend on your industry, average ticket price, volume & business type.

The task of finding just the right mobile payment processing solution can be so overwhelming, so we’ve put together this guide to remove some of your apprehension and help you figure out which is best for you.

You will be able to see information on:

Let's Get You Started!

Understanding how Credit Card Processing can work for you!

The Complete Guide to Credit Card Processing is an in-depth explanation of how credit card processing works. This guide will help you evaluate and decide on the best merchant account without the false starts and missteps that others have fallen prey to in the past. Download your copy of the world's most-comprehensive guide on credit card processing.

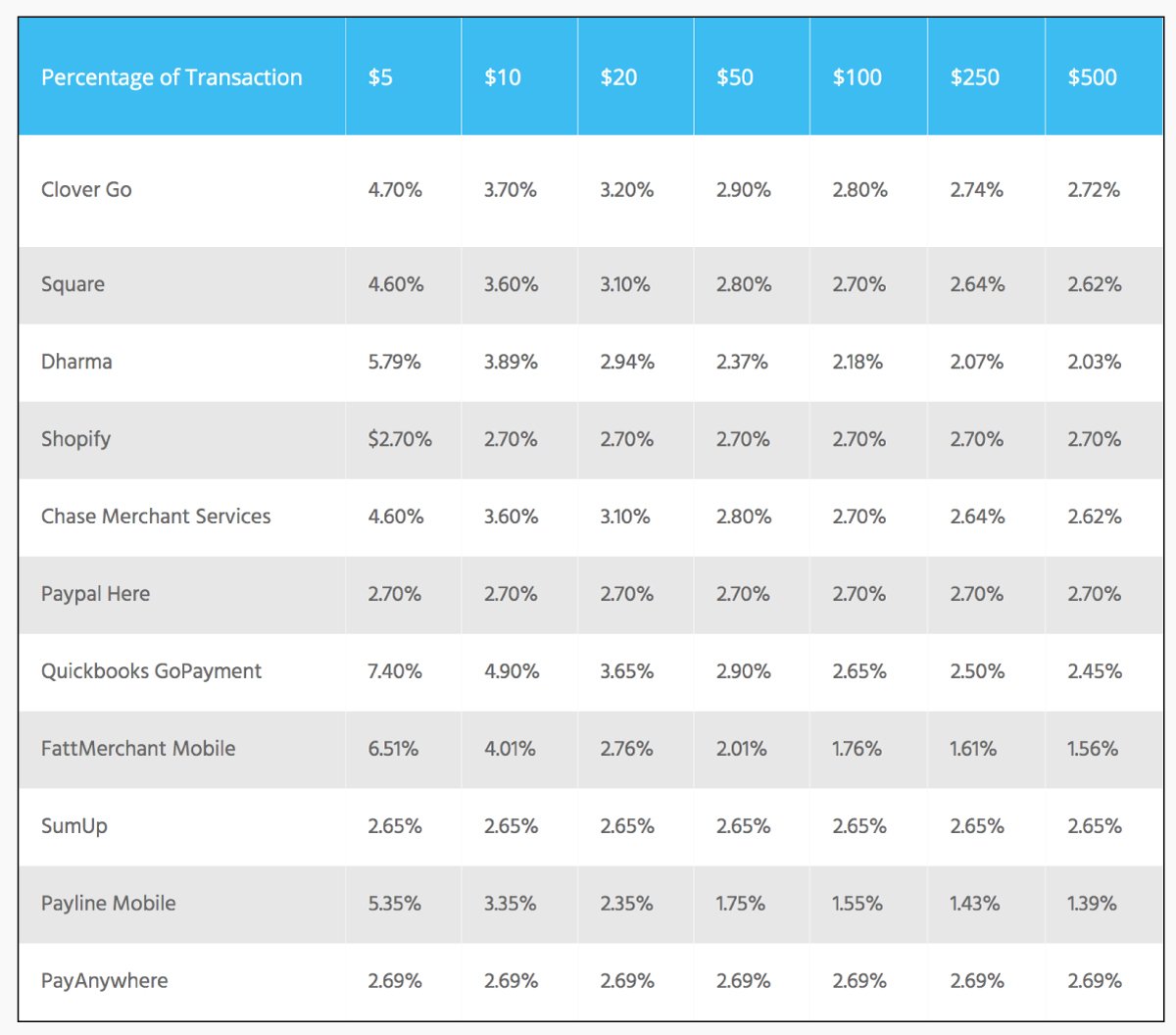

3.1 Just Show Me The Numbers

So you're interested in just the numbers? Awesome.

The charts below show the cost per transaction for each of the top 11 processors as advertised on their websites. The top table shows information on your average ticket sale and you can see what the transaction fees actually would be for that size transaction. For instance, out of a $5 transaction with Clover, $0.24 of that will go to Clover instead of you. The table below tells what percentage of that transaction will cost you with each of these processors - so our $5 transaction with Clover comes out to 4.70%.

Some things to note- this does not include any monthly fees that you might pay to these processors, which can vastly affect your overall cost. For our interchange plus processors (Dharma, Fatt Merchant, and Payline Mobile), we used the 2019 Visa CPS retail interchange rates as a means to compare vendors.

Cost Per Transaction | $5 | $10 | $20 | $50 | $100 | $250 | $500 |

|---|---|---|---|---|---|---|---|

Clover Go | $0.24 | $0.37 | $0.64 | $1.45 | $2.80 | $6.85 | $13.60 |

Square | $0.23 | $0.36 | $0.62 | $1.40 | $2.70 | $6.60 | $13.10 |

Dharma | $0.29 | $0.39 | $0.59 | $1.19 | $2.18 | $5.17 | $10.14 |

Shopify | $0.14 | $0.27 | $0.54 | $1.35 | $2.70 | $6.75 | $13.50 |

Chase Merchant Services | $0.23 | $0.36 | $0.62 | $1.40 | $2.70 | $6.60 | $13.10 |

Paypal Here | $0.14 | $0.27 | $0.54 | $1.35 | $2.70 | $6.75 | $13.50 |

Quickbooks GoPayment | $0.37 | $0.49 | $0.73 | $1.45 | $2.65 | $6.25 | $12.25 |

FattMerchant Mobile | $0.33 | $0.40 | $0.55 | $1.01 | $1.76 | $4.03 | $7.80 |

SumUp | $0.13 | $0.27 | $0.53 | $1.33 | $2.65 | $6.63 | $13.25 |

Payline Mobile | $0.27 | $0.34 | $0.47 | $0.88 | $1.55 | $3.58 | $6.95 |

PayAnywhere | $0.13 | $0.27 | $0.54 | $1.35 | $2.69 | $6.73 | $13.45 |

Shift Processing | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

Percentage of Transaction | $5 | $10 | $20 | $50 | $100 | $250 | $500 |

|---|---|---|---|---|---|---|---|

Clover Go | 4.70% | 3.70% | 3.20% | 2.90% | 2.80% | 2.74% | 2.72% |

Square | 4.60% | 3.60% | 3.10% | 2.80% | 2.70% | 2.64% | 2.62% |

Dharma | 5.79% | 3.89% | 2.94% | 2.37% | 2.18% | 2.07% | 2.03% |

Shopify | $2.70% | 2.70% | 2.70% | 2.70% | 2.70% | 2.70% | 2.70% |

Chase Merchant Services | 4.60% | 3.60% | 3.10% | 2.80% | 2.70% | 2.64% | 2.62% |

Paypal Here | 2.70% | 2.70% | 2.70% | 2.70% | 2.70% | 2.70% | 2.70% |

Quickbooks GoPayment | 7.40% | 4.90% | 3.65% | 2.90% | 2.65% | 2.50% | 2.45% |

FattMerchant Mobile | 6.51% | 4.01% | 2.76% | 2.01% | 1.76% | 1.61% | 1.56% |

SumUp | 2.65% | 2.65% | 2.65% | 2.65% | 2.65% | 2.65% | 2.65% |

Payline Mobile | 5.35% | 3.35% | 2.35% | 1.75% | 1.55% | 1.43% | 1.39% |

PayAnywhere | 2.69% | 2.69% | 2.69% | 2.69% | 2.69% | 2.69% | 2.69% |

Shift Processing | 0% | 0% | 0% | 0% | 0% | 0% | 0% |

We want to tell you how we evaluated these mobile credit card processing companies before we get into the nitty gritty of the individual processors. Each of the options below were evaluated based on the following: overall price, ease of use, POS app, its simplicity, reliability and its ability to integrate with other sales channels that you might have.

We know at the end of the day, it comes down to your profit. You know that accepting credit cards can increase business & that processing them is part of the cost of business. Processing rates, fees, contracts, equipment, software and portability are just some of the things that need consideration as you choose your payment processor.

Want to save this entire guide for later?

We’ve researched 13 credit card processors who also provide mobile processing. Take a look below to see which one interests you.

Who It's Good For:

Customers who are already using Clover systems

Pricing:

Monthly fees start at $14 per month for the use of POS software

Accepts all major credit cards

2.7% +10 cents/transaction for swiped payments,

3.5% + 10 cents transaction for keyed in payments.

Equipment Cost:

$69 for reader, accepts magstripe, chip, NRC plus takes payments like Apple Pay, Google Pay & Samsung Pay

Features:

Also offers:

A full range of payment processors, not just mobile

What's Missing?

The reader only works with Clover, you cannot take it to another processor if you decide to leave Clover.

Reviews:

Inconsistent pricing and bundling, charges fees that similar providers provide for free

Who It's Good For:

Any business that is ready to launch and use mobile credit card processing or any business processing less than $ 3000/month

Pricing:

Flat rate pricing with no membership fee

$0/month for basic plan

Accepts all major credit cards

2.6% +10 cents/transaction for swiped payments

2.9% + 30 cents/transactions for keyed in payments.

Equipment Cost:

Each additional magstripe reader is $10 after the first free card reader

Accepts all major brands of credit cards.

Contactless and chip readers cost $49 dollars. Also able to accept payments like Apple Pay & Google Pay

Features:

Also offers:

A full range of payment processors making it easy to expand as your business grows.

What's Missing?

Cannot accept ACH payments

Reviews:

Most reviews are positive, Square is a solid all around choice for your small business. It has a clear, no surprises pricing structure. The app is easy to use and it’s easy to get started. However, if you are considered “high risk,” they may not be willing to process your payments.

Who It's Good For:

Established businesses that average over $20 per transaction

Pricing:

Subscription fees with interchange plus transaction fees

Starts at $ 20/ month

Visa, Mastercard & Discover 0.15% + $0.07 above interchange per transaction

American Express 0.25% + $0.07 above interchange per transaction

Mobile & virtual processing is included for free through MX Merchant Express

Equipment Cost:

Mobile chip card readers are $99

Features:

Reviews:

Dharma offers low cost rates but are selective about who they will service. It is better for established businesses.

Who It's Good For:

Any business doing at least $5,000 a month in credit card processing.

Pricing:

Mobile Credit Card Processing Fee: $15 per month

Swiped payments: 0%+ 0

Keyed in payments: 0% + 0

Visa, Mastercard, American Express, Discover & rewards cards, Apple Pay & Google Pay

Equipment Cost:

Bluetooth Tap and Chip card reader- free

Features:

What's Missing?

It cannot accept ACH payments. Cannot manage staff. Does not integrate with Quickbooks

Reviews:

Shift offers excellent customer support. This solution is easy to set up and can save business owners thousands of dollars a year because it can zero out their credit card fees.

Who It's Good For:

Great for ecommerce sellers, online store, & retailers looking to expand into accepting in-person mobile payments

Pricing:

Subscription fees with flat transaction fees

Price: Plans start at $29 per month

Swiped payments: 2.7%+ 0

Keyed in payments: 2.9% + 30 cents

Visa, Mastercard, American Express, Discover & rewards cards, Apple Pay & Google Pay

Equipment Cost:

Tap & chip mobile card reader is $49

Features:

What's Missing?

Does not accept payments offline - which is somewhat of a problem for those who want to process payments via mobile card reader.

Reviews:

Shopify offers excellent customer support and easy to integrate with other sales channels. It is really suited for retail sales

Who It's Good For:

Businesses who want to streamline their finances and have it all in one place

Pricing:

2.6% + 10 cents/ swiped or chip transaction*

3.5% + 10 cents/ keyed in transaction*

*Quote based service - make sure you contact a Chase Merchant Services representative for an accurate rate

Equipment Cost:

$95 for bluetooth Chip & swipe reader.

Also have stand alone terminals and e-commerce solutions available

Features:

What's Missing?

The card reader does not have tap functionality.

Reviews:

Do your homework and get a quote with Chase to compare to other pricing models. You may get a better rate depending on the type of business you run. Be sure to ask about other hidden fees so you can get an accurate picture.

Who It's Good For:

If you already use PayPal Business and want to accept payments in person or a new business since it has low start up costs.

Pricing:

Flat fee pricing model, no monthly fee, no contract

Use of the mobile app & compatible smart phone

No monthly fee

2.7%/ swiped, chip or tap transaction

3.5% + $0.15 per keyed in transaction

2.9% + $0.30 per invoiced transaction

Equipment Cost:

$19.99 for magstripe reader (only plugs into phone’s audio jack- may not be compatible with all devices)

$24.99 for EMV card reader

$59.99 for Chip & Tap reader

Features:

Reviews:

Integrates with other PayPal services, but holds & processing are complicated. Many users complain about holding funds. It seems to be only applicable to high risk transactions like keyed-in transactions made on the mobile card reader. Those kind of payments that are beyond $500 are held for 30 days, after which it is deposited into your account. If you use the chip reader, you will get your funds much quicker.

Who It's Good For:

Those who use Quickbooks and want a simple mobile extension to be able to accept payments.

Pricing:

Have to have a QuickBooks online account- which starts at $25 per month (although they advertise the first 3 months are 50% off)

Accepts all major credit cards

Swipe & chip payments: 2.4% + $0.25 /transaction

Keyed in payments: 3.4% +$0.25/ transaction

Invoiced payments: 2.9% + $0.25 / transaction

ACH payment cost: 1% with max of $10

Equipment Cost:

Chip & Magstripe reader $19 or free with QuickBook payments

All in one reader (including EMV & Tap) $49 - takes payments like Apple, Google & Samsung Pay

Both connect via Bluetooth

Features:

Reviews:

The reviews are a mixed bag with this one. While it integrates with Quickbooks, you have to make sure you have the correct plan to be able to get the features you’d like, such as invoicing.

Who It's Good For:

Established businesses that process high-volume and high ticket accounts

Pricing:

Monthly fee: starts at $99 per month (for processing less than $500k annually)

Direct cost interchange fees +$0.15 per transaction

Equipment costs:

Chipper BT: Accept magstripe & chip cards via bluetooth on both iOS or Android devices. (Price not disclosed on their website)

Chipper 2X BT: magstripe, chip cards & ApplePay (Price not disclosed on their website)

Features:

Reviews:

Easy for clients to make payments, integrates with Quickbooks, Great customer service, Simple to use. A solid business to be sure, but can be expensive to use for a small business.

Who It's Good For:

Small business Quick-Serve, Food Truck, Coffee Shop, Retail, Restaurant/Bar

Pricing:

A Quote-based model, you will have to contact Shopkeep to get a price

Pay as you go monthly subscription service

Features:

Reviews:

This software was designed for small businesses, like specialty vendors & local restaurants. The software is easy to use and has up front pricing.

Who It's Good For:

Businesses that travel to conventions, trade shows, and pop-up events

Pricing:

Accepts all major credit cards, Apple Pay & Google Pay

Accept Magstripe, EMV Chip & Tap payments, connects via Bluetooth

Pair with mobile device or tablet

Flat pricing: 2.65%/transaction

Virtual Terminal fee: 2.95% + $0.15

No contracts, no monthly minimums

Equipment Cost:

All-in-one Card Reader $19

Features:

Reviews:

SumUp is an established company, and is good if you want a straight forward card reader and app. It doesn’t have extensive features (like invoicing) that other mobile processors might offer for similar pricing.

Who It's Good For:

They offer many types of pricing models. For a mobile business, you will probably begin with Payline Start.

Pricing:

Payline Start pricing:

Interchange + pricing model + monthly fee

Magstripe, EMV or Contactless: Interchange + 0.2% + $0.10/ transaction as well as $10 per month

Keyed in payments: Interchange + 0.3% + $0.20 per transaction plus $20/month

Equipment Cost:

Payline suggests Clover Go for their mobile card reader - Price to own is $70 plus $11/month (the length of $11/ month is not disclosed)

Features:

Reviews:

Although it is not transparent on their website, many reviewers have complained that Payline a monthly minimum requirement in processing. This is a more expensive option for those businesses that do not process enough credit card volume to offset the $25 monthly fee if you don’t meet the minimum. Also, they are unlikely to service high risk accounts.

Quote-based pricing model & have many options available depending on the type of business you have.

Pricing is not transparent on their website, so it’s best to contact them to get a quote and compare pricing.

Who It's Good For:

If you only do in-person payments and process over $5k/month.

Pricing:

pay 2.69% for swipe, dip or tap payments

Pay 3.49% +0.19 for keyed in manual payments

Invoicing, recurring & virtual terminal payments: 3.49% + $0.19/ transaction

Custom rates if process over 10K/month

Equipment Cost:

2-1 reader: Stripe & EMV chip cards- first one is free. Additional readers $29.95 each

3-1 reader: EMV chip, magstripe cards, NFC contactless payments $49.95 each

Features:

Reviews:

Some reviews say that this is a tiered-pricing model. Make sure if you decide to use this plan that you have a clear understanding of what you are paying.

The processing rate is made up by 2 components:

Interchange+ Pricing - good for most businesses

The merchant pays the true cost on all credit cards and the markup set by the processor. It is the best of the conventional pricing models unless your business has very low volume. If you have less than $2000 a month in credit card purchases, then you’d be better served with another model.

Membership Pricing - good for high volume per tickets

Pay either a monthly or annual fee & businesses receive an interchange pricing model at zero basis points of cost. A small swipe fee will still be incurred, but it usually ranges from $0.03-$0.25 per item. This type of processing model is great for very high average tickets like furniture stores or law firms.

Tiered Pricing - tends to be the most expensive way to process credit cards

Tiered pricing divides all card types into three tiers: qualified &mid-qualified & non-qualified. However, this is a tactic used by the credit card processors. The credit card issuers (Visa, Mastercard, Discover and Amex) have not made any statements whether any of their cards fall into any of these categories. It’s made up! It will be the most expensive way to run your business.

Flat Rate - good for low volume tickets & mobile processing

The processing rate is a flat fee per transaction. These are great for businesses with a low ticket average of $5 or less, or process less than $2000 a month.

Zero Fee

The processing fee is placed on the customer. The customer can pay with cash for a discounted rate, or conveniently pay with a credit card with the cost of using the credit card added on. Usually the fee is so nominal that the customer doesn’t mind paying it, and the business isn’t losing money in processing fees.

The processing rate is determined by the issuing banks, credit card companies & merchant service provider. This is what you (the business) will pay per transaction.

Processing fees are an additional cost on top of the processing rate for the service that gets money from one bank (the customers) to the other (to yours). These include the discount rate, the swipe fee, batch processing fee, PCI, statement fee, annual fees, monthly minimum fee, early termination fee, card network fees, AVS fees, voice authorization fee if you have to all in a credit card number, retrieval request fees should a customer dispute a charge from your business. See chapter 1 of this guide for a more in depth look at processing fees.

While the processing rates are described above, the fees described below are not included in the price per transaction fee. These are additional fees you will probably incur unless your merchant service provider specifically says they don’t charge for these things.

An early termination fee is a fee that the processor imposes on the merchant (business) if they decide to cancel their processing contract. This is to offset the money they will lose since you won’t be processing with them anymore. It can be thousands of dollars and a huge headache. Avoid this by reading your contract thoroughly and ensuring there are no early termination fees.

A monthly fee is basically a made up fee that the processing company decided to make mandatory. There are no required fees from the card brands or issuing banks. It’s just a way for the processor to make more money off of you.

A monthly minimum refers to the minimum amount of sales that you must have as a merchant. If you fail to hit the minimum required credit card transactions, you will incur a fee to guarantee that the processor will make a minimum amount of money each month. You can avoid it by ensuring you are making enough credit card sales, or by choosing a credit card processor that does not have this fee.

PCI Compliance means that businesses follow the Payment Card Industry Data Security Standard. This fee can range from $6-$25 monthly or $99-$199 annually. This fee can be avoided though. All you have to do is fill out the PCI Compliance form with your processor. Your processor will submit your account as PCT compliant and there won’t be a fee. Make sure you ask your processor to do this for you.

A statement is a record that contains all the monthly credit card transactions and fees paid by the merchant. It is a written record, usually available electronically as well. These fees can range from $5-$20/month and some companies charge an extra fee to be able to view this electronically.

A contract is a way for processors to lock the merchant in for many years. This way, they have guaranteed years of processing. If a merchant were to leave, then the processor will charge hundreds, if not thousands, of dollars. This guarantees their own profit on that particular account.

Month to month contracts (pay as you go) contracts are great for the business owner because you have the option to cancel at any time. Month-to-month contractors want to keep you with them, so they will work hard to make sure you are happy with excellent customer service and lower costs.

Be advised that some month-to-month processors’ equipment and mobile POS software are only compatible with their brand. For example, If you decide to leave Square for a different processor (Clover Go), you will have to purchase new equipment and software to keep your business running. Clover Go will run off their own equipment and software.

Annual contracts are a bad idea for any business- they are only good for the merchant processor. They can make lots of money off of you, and if you’re not happy with them- too bad, you’re stuck! This can be very expensive and lock you into something that might not be good for you for a whole year. As a business owner, walk away whenever presented with multi-annual contracts.

There are several different types of mobile credit card readers that can be used to take payments, which we have listed below. But a word of caution: although some providers have month-to-month contracts, their card reader can only be used with their POS system. If you decide to go with a different mobile processor, you may end up spending more money for compatible equipment and software.

Wireless Terminals

Square & Clover Go offer stand alone terminals, but there are other options available. If you want to use a wireless terminal without your smartphone, be sure it integrates with your POS software if you’re not using a mobile processor specific one.

Mobile Card Magstripe Readers

Magstripe readers only take swipe cards. They pair with a smart phone or tablet and specific mobile app. Some may need to be connected to wi-fi or use cellular data to take payments

Mobile Card EMV Chip Readers

Chip or “Dip” reader that pairs with a smart phone or tablet and specific app. The EMV credit card provides more security because of the chip-reader technology.

Mobile Card Contactless Readers

Pairs with a smart phone or tablet & specific app - accepts “tap” or “wave” technology as well as Apple Pay, Google Pay.

We hope this gave you a solid overview of what mobile credit card processing entails and what is out there. As you can see there are a lot of moving parts in making your decision - your business type, your average ticket price, your monthly volume of sales, POS system, hardware, portability, and if you need other functions like employee & inventory management.

And be aware, when you are choosing a mobile processor, do the math and compare them for yourselves. Sure, a processor might have a really low fee, but do they charge a monthly subscription fee or a fee if you don’t process enough with them? Always look at the big picture and determine what it will actually cost you.

Still unsure about what kind of mobile processor you should use? We at Shift Processing would be happy to talk with you to point you in the right direction.

Chapter 1

How to Avoid Credit Card Processing Fees

Chapter 2

Online Credit Card Processing: No Storefront, No Problem, right?

Chapter 3

Accepting Mobile Credit Card Processing Payments on the Go

Chapter 4

High Risk Merchant Account: Can I accept domestic payments with no reserves?

Chapter 5

Choosing the Credit Card Processing for Small Business That’s Right for You

Chapter 6

Credit Card Processing Companies: We Compare the Industry Leaders

Chapter 7

The Best Credit Card Processing: Find a Partner that will Lower Your Rates

Follow us

company

Statistics

Features

resources

how it works

Equipment

Copyright 2026 | Shift Processing | All Rights Reserved | Indianapolis Web Design by Fusion Creative